Review of Hatton National Bank PLC (HNB) Financial Performance for the Three Months Ended 31st March 2025

1. Executive Summary:

Hatton National Bank (HNB) demonstrated strong financial performance in the first quarter of 2025, setting a solid foundation for future growth. The Bank and Group reported significant increases in Profit After Tax (PAT), primarily driven by improved net interest income and a surge in other income, particularly foreign exchange gains due to Sri Lankan rupee depreciation. Asset quality continued to improve with a lower Net Stage 3 ratio and increased coverage. HNB also strengthened its position as a diversified financial services conglomerate through strategic investments and maintained robust capital and liquidity buffers well above regulatory requirements. The Bank received a credit rating upgrade and significant industry accolades during or immediately preceding the quarter.

2. Key Financial Highlights (Q1 2025 vs Q1 2024):

- Profitability:Group PAT: Rs 11.1 Bn, a 49% YoY growth.

- Bank PAT: Rs 10.2 Bn, a 64% YoY growth.

- “HNB continued its growth trajectory in Q1 2025, recording a YoY growth of 49% in Group Profit After Tax (PAT) and a 64% growth in Bank PAT with Group and Bank PAT at Rs 11.1 Bn and Rs 10.2 Bn, respectively.”

- Net Interest Income (NII):Bank NII: Grew by 7.7% YoY to Rs 23.7 Bn.

- Growth achieved despite lower interest rates due to a higher rate of decrease in interest expenses (27.1% YoY) compared to interest income (14.4% YoY), supported by growth in CASA deposits.

- “Bank’s Net Interest Income (NII) grew by 7.7% YoY to Rs 23.7 Bn during the first quarter in the backdrop of lower interest rates compared to the corresponding period of 2024.”

- Non-Interest Income:Net fee and commission income: Increased by 17.0% YoY, driven by higher card usage and digital transactions.

- Other income (largely exchange income): Surged to Rs 2.3 Bn, compared to a loss of Rs 2.1 Bn in Q1 2024, primarily due to Sri Lankan rupee depreciation.

- “Net fee and commission income experienced a 17.0% YoY increase, largely driven by higher card usage and a surge in digital transactions…”

- “…other income comprising largely of exchange income surged to Rs 2.3 Bn, mainly due to the depreciation of the Sri Lankan rupee. From a loss of Rs 2.1 Bn recorded in the corresponding period of 2024.”

3. Asset Quality and Risk Management:

- Improved Asset Quality: Asset quality continued to show notable improvement due to robust risk management and intensified recovery efforts.

- Net Stage 3 Ratio: Improved to 1.82% as at March 31, 2025, from 1.88% as at December 31, 2024.

- “Asset quality continues to improve further with Net Stage 3 ratio at 1.82%”

- Stage 3 Coverage Ratio: Strengthened to 75.12% as at March 31, 2025.

- “…the Stage 3 coverage ratio strengthened to 75.12%.”

- Impairment: Recorded a total impairment reversal of Rs 379.7 Mn in Q1 2025, compared to a charge of Rs 1.4 Bn in Q1 2024.

- “…the Bank witnessed a positive movement in its stage 3 portfolio resulting in a total impairment reversal of Rs 379.7 Mn, compared to a charge of Rs 1.4 Bn in the corresponding period last year.”

4. Strategic Developments:

- Investment Banking Integration: Completed the acquisition of the remaining 50% stake in HNB Investment Bank (formerly Acuity Partners (Pvt) Ltd) from DFCC PLC for Rs 6.5 Bn on January 21, 2025. This entity is now a wholly-owned subsidiary and has been rebranded.

- “Integrates the fully owned investment banking business under the group”

- “On January 21, 2025, HNB PLC acquired 75,500,001 ordinary voting shares, representing a 50% stake held by DFCC Bank PLC in Acuity Partners (Pvt) Ltd, for a consideration of Rs 6.5 Bn.”

- HNB Finance PLC: Participated in HNB Finance PLC’s rights issue, further solidifying HNB’s standing as a diversified financial services conglomerate.

- “…took part in HNB Finance PLC’s rights issue—further solidifying its standing as the most diversified financial services conglomerate in the Country.”

5. Capital Adequacy and Liquidity:

- Strong Capital Buffers: Maintained strong capital buffers well above regulatory minimums despite strategic investments.

- Tier 1 Capital Adequacy Ratio (Bank): 17.60% (Regulatory minimum: 9.5%).

- Total Capital Adequacy Ratio (Bank): 21.89% (Regulatory minimum: 13.5%).

- “Despite these strategic investments, the Bank maintained strong capital buffers with Tier 1 and Total Capital Adequacy ratios at 17.60% and 21.89%, respectively, well above the minimum statutory requirements of 9.5% and 13.5%.”

- Strong Liquidity Position: Maintained a strong liquidity position.

- All currency Liquidity Coverage Ratio: 364.49% (Regulatory minimum: 100%).

- “Additionally, the Bank maintained a strong liquidity position, with an all currency Liquidity Coverage Ratio of 364.49%, well above the regulatory minimum requirement of 100%.”

6. Recognition and Ratings:

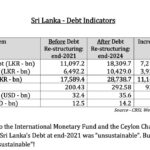

- Credit Rating Upgrade: Fitch Ratings Lanka Ltd upgraded HNB’s credit rating to AA-(lka) in January 2025 following the completion of the external debt restructuring program.

- “Following the completion of the external debt restructuring program, Fitch Ratings Lanka Ltd upgraded HNB’s credit rating to AA-(lka) as part of the rating recalibration in January 2025.”

- Industry Accolades: Honored as the ‘No. 1 Corporate in Sri Lanka’ in the ‘Business Today Top 40’ rankings in 2024 and named the ‘Best Retail Bank in Sri Lanka’ by The Asian Banker for the 15th time.

- “In 2024, HNB was honoured as the ‘No. 1 Corporate in Sri Lanka’ in the ‘Business Today Top 40’ rankings. Other significant accolades include being named the ‘Best Retail Bank in Sri Lanka’ by The Asian Banker, marking the 15th occasion the Bank has received this coveted title.”

7. Key Financial Figures (Unaudited – As at March 31, 2025):

- Total Assets (Group): Rs 2,149.9 Bn (increase of 3% from Dec 31, 2024).

- Total Assets (Bank): Rs 2,356.3 Bn (increase of 7% from Dec 31, 2024).

- Total Liabilities (Group): Rs 1,916.8 Bn (increase of 4% from Dec 31, 2024).

- Total Liabilities (Bank): Rs 2,080.5 Bn (increase of 7% from Dec 31, 2024).

- Total Equity (Group): Rs 233.1 Bn (increase of 1% from Dec 31, 2024).

- Total Equity (Bank): Rs 275.8 Bn (increase of 2% from Dec 31, 2024).

- Net Assets Value per ordinary share (Voting): Rs 407.75 (increase of 1% from Dec 31, 2024).

- Gross loans and advances to customers (Group): Rs 1,174.1 Bn.

- Gross loans and advances to customers (Bank): Rs 1,227.3 Bn.

- Due to depositors (Group): Rs 1,723.2 Bn.

- Due to depositors (Bank): Rs 1,760.1 Bn.

8. Other Notable Information:

- No changes in accounting policies or methods of computation since the 2024 annual accounts.

- No material changes in assets, liabilities, contingent liabilities, or use of funds from debentures during the period.

- Debenture issues from 2024 were fully utilized for strengthening Tier 2 capital and facilitating future business expansion.

- A final cash dividend of Rs 15/- per share on both voting and non-voting shares for 2024 was approved at the AGM on March 27, 2025.

- Director Mr. T. P. P. L. Rodrigo is resigning with effect from May 30, 2025.

- Segment reporting is provided for various business areas including Corporate, Retail, SME, Micro, Real Estate, Insurance, NBFI, Treasury, and Investment Banking.

9. Shareholding Information:

- Top 20 Major Shareholders (Voting and Non-Voting) are listed, with Browns Investments PLC holding the largest stakes in both categories.

- Certain major shareholders in the Voting category (Milford Exports, Stassen Exports, Distilleries Company of Sri Lanka) have their collective voting rights limited to 10% as per Banking Act Directions.

10. Fair Value of Financial Instruments:

- The report provides a detailed breakdown of financial assets and liabilities measured at fair value (Level 1, 2, and 3) and those carried at amortized cost.

- A significant portion of financial assets measured at amortised cost, such as loans and advances to customers and debt/other financial instruments, are presented with their fair values, generally valued using significant observable inputs (Level 2).

11. Conclusion:

HNB’s Q1 2025 results indicate a strong start to the year, characterized by robust profit growth, improving asset quality, strategic expansion in investment banking, and maintenance of healthy capital and liquidity levels. The positive financial performance, coupled with the credit rating upgrade and industry recognition, positions HNB favorably for continued success