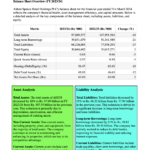

Financial Performance

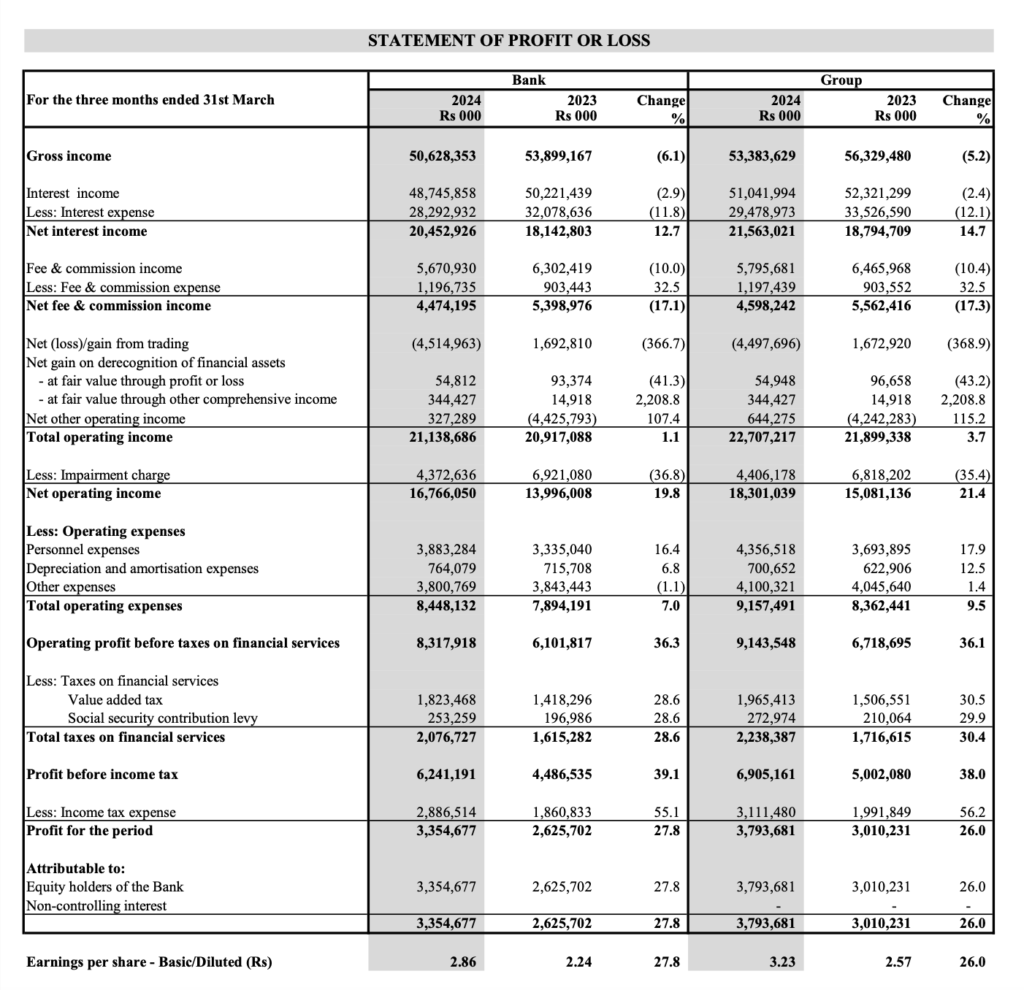

Sampath Bank posted a profit before tax (PBT) of Rs 6.2 Bn and a profit after tax (PAT) of Rs 3.4 Bn for the three months ended 31st March 2024, notwithstanding an exchange loss of Rs 4.3 Bn due to the appreciation of LKR against USD by Rs 23.70. These figures signify growth rates of 39.1% and 27.8% respectively, in comparison to the financial results reported in the first quarter of 2023. The Sampath Group also reported PBT and PAT figures of Rs 6.9 Bn and Rs 3.8 Bn respectively, reflecting growth rates of 38.0% and 26.0%

Key highlights for the period ended 31st March 2024

- A significant increase of 27.8% in the Bank’s PAT bringing it to Rs 3.4 Bn.

- 12.7% growth in Net Interest Income (NII).

- 17.1% decrease in net fee and commission income due to decreased trade-related operations.

- An exchange loss of Rs 4.3 Bn due to the appreciation of LKR against USD by Rs 23.70.

- 36.8% decline in impairment charges.

- Robust LKR deposit growth of Rs 68 Bn.

- Tier 1 and Total Capital Adequacy Ratios stood at 15.18% and 18.22% respectively as at 31stMarch 2024, comfortably remaining above regulatory minimum requirements.

Fund based income

During the period, Net Interest Income (NII) reached Rs 20.5 Bn, marking a growth of 12.7% compared to Rs 18.1 Bn recorded in the corresponding period of the previous year. This increase in NII primarily stemmed from a reduction in interest expense which outpaced the decrease in interest income.The Bank’s prudent asset and liability management strategies played a pivotal role in driving the notable growth of NII, especially amid declining interest rates. Additionally, the Net Interest Margin (NIM) witnessed an increase, rising from 5.16% as of 31st December 2023, to 5.24% as of the reporting date.

Non-Fund based income

In 1Q 2024, the Bank experienced a significant 75.3% decrease in its total non-fund based income, declining from Rs 2.8 Bn reported in the corresponding period of last year to Rs 0.7 Bn in the current period. Net fee and commission income recorded a 17.1% decrease compared to 1Q 2023, primarily due to reduced income from trade-related activities. The decline was driven by several factors including lower commission rates for import-related transactions, decreased trade volumes and the appreciation of LKR against the USD. However, fees generated from credit, electronic channels, cards and remittance-related activities showed growth compared to the same period last year.The Bank reported a net trading loss of Rs 4.5 Bn in 1Q 2024 whereas there was a gain of Rs 1.7 Bn recognized in the previous period. This was primarily due to revaluation losses incurred on forward exchange contracts. The Bank managed to mitigate the impact of this loss through realized exchange gains reported under net other operating income as opposed to the loss of Rs 4.5 Bn recorded in 1Q 2023. Consequently, the Bank’s net exchange loss from foreign exchange operations for the period under review amounted to Rs 4.3 Bn, compared to the Rs 2.9 Bn loss reported in the corresponding period of the previous year.

Impairment Charge

In the first quarter of 2024, the Bank reported a total impairment charge of Rs 4.4 Bn, a 36.8% decrease compared to the charge for the comparative period in the previous year. Of this total, Rs 2.4 Bn was attributed to loans and advances (1Q 2023: Rs 6.2 Bn), while Rs 0.9 Bn related to other financial instruments (1Q 2023: Rs 0.4 Bn). In addition, an impairment charge of Rs 1.1 Bn was recorded for commitments and contingencies (1Q 2023: Rs 0.4 Bn).

Impairment charge on loans and advances

The Bank witnessed a 61.5% reduction in the impairment charge against loans and advances. This decrease can be attributed to the effectiveness of the Bank’s prudent provisioning policies implemented in previous years and the revival of economic activities resulting in enhanced credit quality of customers.

During the first quarter of 2024, the Bank conducted a thorough assessment of individually significant customers (ISL) and made tailored provisions in the Financial Statements, accounting for the specific risk factors associated with them. During this period, the Bank observed a reversal in collective impairment indicating an encouraging trend in economic activity and resulting enhancements in customer credit quality. The Bank maintained allowances for overlays for segments with elevated credit risk in line with year-end 2023 practices with most overlays persisting throughout 1Q 2024. Furthermore, the basic impairment models used for collective impairment in 2023 remained unchanged, ensuring sufficient buffers to mitigate potential future credit risks.

Impairment charge on other financial instruments

The Bank recorded a net impairment charge of Rs 0.9 Bn against other financial instruments during 1Q 2024 primarily due to the recognition of an additional charge against Sri Lanka International Sovereign Bonds (SLISB).

Operating Expenses

In the reporting period, operating expenses saw a 7.0% increase compared to the first quarter of 2023. The increase in personnel costs by 16.4% was primarily driven by the annual salary increments. As a result, the Bank’s cost-to-income ratio increased by 230 basis points, from 37.7% in 1Q 2023 to 40.0% in 1Q 2024. The negative impact on the Cost to Income ratio can be attributed to both numerator and the denominator, an uptick in operating expenses during the period as well as a decrease in revenue due to exchange losses.

Taxation

The Bank’s total effective tax rate rose to 59.7% in the first quarter of 2024 from 57.0% reported in the corresponding period in 2023.

Key Ratios

The Return on Average Shareholders’ Equity (after tax) was 9.04% as of 31st March 2024, down from 12.65% reported as of 31st December 2023. Similarly, the Return on Average Assets (before tax) stood at 1.59% as of 31st March 2024, compared to 2.12% reported at the end of 2023.

Capital and Liquidity

Throughout the review period, Sampath Bank maintained all its capital ratios comfortably above regulatory minimum requirements. As of 31st March 2024, the Bank’s CET 1, Tier 1, and total capital ratios were at 15.18%, 15.18%, and 18.22%, respectively, compared to 16.35%, 16.35%, and 19.56% recorded at the end of 2023. The change in capital ratios during the reporting period can be attributed to two primary factors: a decrease in capital resulting from the distribution of retained earnings to pay a cash dividend of Rs 6.9 Bn and an increase in risk-weighted assets stemming from loan growth during the period.

Assets

The Bank’s asset base grew by 5.8% (annualized growth of 23.3%) from Rs 1.54 Tn as of 31st December 2023 to Rs 1.63 Tn as of 31st March 2024. This expansion was driven by increased investment in Government debt securities and growth in the loan book. Investments in LKR T-bills

and T-bonds collectively increased by Rs 78 Bn, while investments in US Treasuries rose by Rs 28 Bn (USD 98 Mn) during the period under review. Furthermore, total gross loans also increased by Rs 18 Bn, from Rs 877 Bn as of 31st December 2023 to Rs 895 Bn at the end of the reporting period. LKR- denominated loans increased by Rs 20 Bn, while foreign currency loans declined by Rs 2 Bn due to the appreciation of LKR against the USD during the period.

Liabilities

Total liabilities grew by 6.5% (annualized growth of 26.1%), primarily driven by the expansion of the Bank’s deposit base, which increased from Rs 1,264.5 Bn at the end of 2023 to Rs 1,331.2 Bn as of 31st March 2024. As of the reporting date, the Bank’s CASA ratio stood at 33.6%, reflecting a slight improvement compared to 33.4% at the end of the previous year. The Bank redeemed debentures issued in 2019, amounting to Rs 7.0 Bn, upon maturity during February 2024.

Dividend

At the Annual General Meeting held on 28th March 2024, the shareholders of Sampath Bank approved a first and final Cash Dividend of Rs 5.85 per share for the financial year 2023. In the 1Q 2024 Financial Statements, the Bank made a provision of Rs 6.9 Bn to facilitate the payment of the approved final dividend to its shareholders.