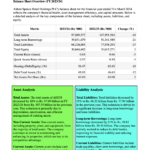

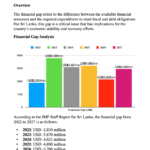

Corporate analysis of Watawala Plantations PLC, we will first look at the net profit figures and profit before tax from the provided interim financial statements for the periods ending in June 2023, September 2023, and December 2023. Here’s a detailed analysis:

Profitability

June 2023: (3 months)

- Profit before tax: LKR 874,752,000

- Net profit for the period: LKR 794,526,000

- Basic Earning per share (LKR): 3.91

September 2023: (6 months)

- Profit before tax: LKR 1,811,066,000

- Net profit for the period: LKR 1,685,023,000

- Basic Earning per share (LKR): 8.29

December 2023: (9 months)

- Profit before tax: LKR 2,203,296,000

- Net profit for the period: LKR 2,203,296,000

- Basic Earning per share (LKR): 10.82

Comparative Analysis:

- The profit before tax from June to September 2023 increased by LKR 936,314,000, indicating a significant improvement in profitability.

- However, the profit before tax from September to December 2023 decreased by LKR 607,770,000, showing a decline in profitability towards the end of the year.

- The net profit also followed a similar trend, with an increase from June to September and then a decrease from September to December.

- The basic earnings per share increased from June to December, which is a positive sign for shareholders.

Key Indicators

- Revenue: The group-level revenue for the nine months ending 31st December 2023 was LKR 6,483 million, which is a decrease of 2.5% year-over-year (YoY).

- Palm Oil Sector Revenue: Specifically, the palm oil sector’s revenue was LKR 5,395 million, down by 6.4% YoY. This decline was attributed to a drop in price, although sales volume increased during the period.

- Profit Before Income Tax: For the quarter ended 31st December 2023, the profit before income tax was LKR 627,997,000, which is a 10% decrease compared to the same period in the previous year.

- Income Tax Expenses: The income tax expenses for the quarter increased by 40% to LKR 53,926,000.

- Profit for the Period: The profit for the period was LKR 574,071,000, a 13% decrease from the previous year’s same quarter.

- Profit Attributable to Equity Holders: The profit attributable to equity holders of the parent for the period was LKR 568,190,000.

- Non-controlling Interests: There was a profit of LKR 5,881,000 attributable to non-controlling interests.

- Dividends: According to the annual report as of 31st March 2023, the dividend per share was LKR 14.00, which indicates a dividend payout ratio of 122%.

- Earnings Per Share (EPS): The EPS as of 31st March 2023 was LKR 11.49.

From this data, we can conclude that Watawala Plantations PLC experienced a decrease in profitability in the quarter ended 31st December 2023 compared to the previous year. The decline in palm oil prices affected the revenue, and despite an increase in sales volume, it was not enough to offset the price impact. The increase in income tax expenses also contributed to the reduced net profit. However, the company maintained a high dividend payout ratio as of the last annual report, which could be a sign of confidence in its long-term profitability or a commitment to returning value to shareholders.

Key Financial Ratios

Financial ratios for Watawala Plantations PLC as at 31st December 2023:

- Net Assets per Share: LKR 29.73 for the Group and LKR 31.05 for the Company, as indicated in the interim condensed financial statements.

- Current Ratio and Quick Asset Ratio: These ratios are not directly provided for the specific date of 31st December 2023. However, we can infer from the context that as of 31st March 2023, the quick asset ratio was 1.86 times for the Group and 2.91 times for the Company, and the liquidity position was healthy. Unless there were significant changes in the current assets and liabilities, we might expect similar liquidity ratios for 31st December 2023.

- Debt-to-Equity Ratio: The debt-to-equity ratio as of 31st March 2023 was 0.04 times for both the Group and the Company. If the company’s financial structure remained relatively stable, the debt-to-equity ratio as of 31st December 2023 might be expected to be in the same range.

Watawala Plantations PLC showed a fluctuating profitability trend over the six months from June to December 2023. While there was an initial increase in profitability from June to September, there was a subsequent decrease towards the end of the year. The Palm Oil segment remains the strongest, while other segments have negatively impacted the company’s profitability. The increase in tax expenses also played a role in reducing the net profit. It’s important for potential investors or stakeholders to consider these trends and factors when making decisions related to the company.

This Analysis was compiled by LankaBIZ (AI Assistant) based on publicly available information. Click below link to Chat with LankaBIZ AI to find answers to queries relating Sri Lanka economy, Business regulations, Corporate Analysis & Stock Market Research.

www.lankabizz.net

Sectors Analysis

The sector analysis of Watawala Plantations PLC, based on the provided context, can be summarized as follows:

Palm Oil Sector:

- Revenue for 6 months ending 30th September 2023: LKR 3,910 million, which was a decrease of 3.2% Year-over-Year (YoY) due to a drop in price, despite an increase in sales volume during the period.

- Revenue for 9 months ending 31st December 2023: LKR 5,395 million, down 6.4% YoY, with the decrease attributed to a drop in price while sales volume increased.

- Annual Revenue for the year ended 31st March 2023: LKR 7,573,816 thousand, which was an increase from the previous year’s revenue of LKR 5,782,074 thousand.

- Gross Profit for the year ended 31st March 2023: LKR 3,743,089 thousand, compared to LKR 3,532,435 thousand in the previous year.

Dairy Sector:

- Annual Revenue for the year ended 31st March 2023: LKR 1,194,790 thousand, up from LKR 693,988 thousand in the previous year.

- Gross Loss for the year ended 31st March 2023: LKR (168,674) thousand, which was a larger loss compared to LKR (26,xxx) thousand in the previous year (the exact figure for the previous year is not fully visible in the context provided).

Other Segments:

- No revenue or profit figures are provided for other segments in the context.

Overall Performance:

- The palm oil sector is the main revenue generator for Watawala Plantations PLC, showing significant growth in annual revenue but experiencing a decrease in revenue in the shorter term due to price drops.

- The dairy sector shows revenue growth year-over-year but is operating at a loss, with the loss increasing in the year ended 31st March 2023 compared to the previous year.

- The company’s overall performance in the palm oil sector appears to be strong in terms of annual revenue growth, despite short-term challenges with pricing. The dairy sector, while growing in revenue, is facing challenges in terms of profitability.

Share Price

The share price and market performance for Watawala Plantations PLC (WATA.N0000) on the Colombo Stock Exchange were as follows:

- The last traded price was LKR 88.00.

- The day’s trading range was LKR 86.90 to LKR 88.50.

- The 52-week range was LKR 67.80 to LKR 94.50.

- The market capitalization was LKR 17.89 billion.

- The volume of shares traded was 121.61K, compared to the 65-day average volume of 80.36K.

For the most current share price and market performance, please refer to the latest data available on financial news platforms or directly from the Colombo Stock Exchange, as these figures are subject to change with ongoing trading activity.

Future Prospects

Future prospects of Watawala Plantations PLC can be inferred as follows:

Palm Oil Sector:

- Stabilization of Global Palm Oil Prices: It is mentioned that global palm oil prices have stabilized, which suggests that the company may not face significant price volatility in the near term.

- Domestic Demand: There is an expectation that domestic demand for palm oil will gradually increase with the recovery of the economy. This could lead to higher sales volumes for the company.

- Impact of VAT: The imposition of Value Added Tax (VAT) on palm oil is noted, but the expectation is that prices will remain stable. The company will need to manage the impact of VAT on its pricing and profitability.

Dairy Sector:

- Milk Yield: Watawala Dairy Ltd (WDL), which is a significant part of the company’s dairy sector, is expected to sustain milk yield due to better management and stockholding of cattle feed.

- Demand for Fresh Milk: Despite the imposition of VAT on fresh milk, demand is expected to remain stable. This indicates that the company anticipates a steady market for its dairy products.

General Outlook:

- Economic Recovery: The company’s prospects are tied to the broader economic recovery, which could enhance demand for its products.

- Management and Efficiency: The company’s focus on better management practices and capturing real-time data for decision-making suggests an ongoing effort to improve operational efficiency and productivity.

Conclusion:

Watawala Plantations PLC appears to be positioned to navigate the challenges posed by taxation changes and is looking to capitalize on stable pricing and increased demand in both the palm oil and dairy sectors. The company’s emphasis on management efficiency and data-driven decision-making is likely to support its future growth and stability. However, it is important to monitor the economic conditions and regulatory changes that could impact the company’s performance.